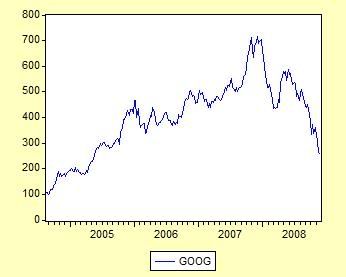

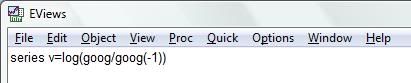

- Jednotkový koreň zamietame, preto na ARMA modelovanie použijeme priamo časový rad v.

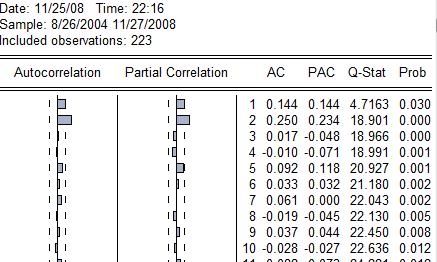

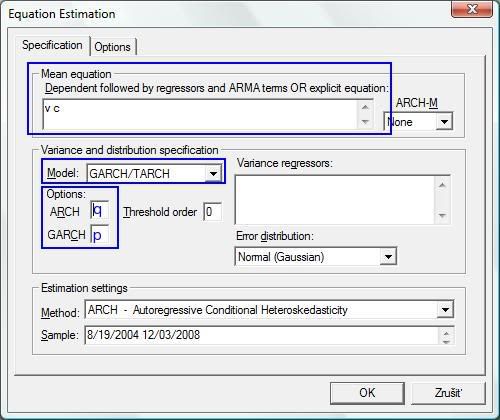

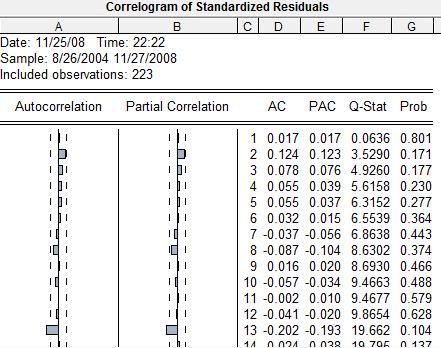

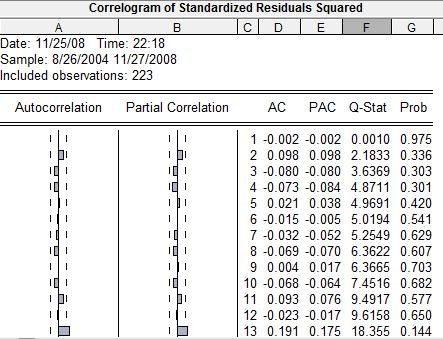

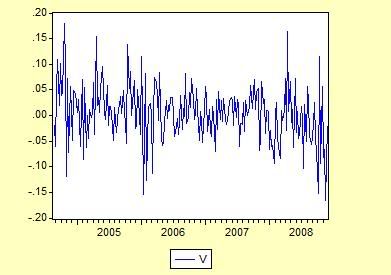

- Autokorelácie a parciálne autokorelácie nie sú signifikantné. Q štatistika nezamieta hypotézu, že v časovom rade nie je autokorelácia.Zdá sa teda, že výnos je konštanta plus biely šum. Odhadneme tento model:

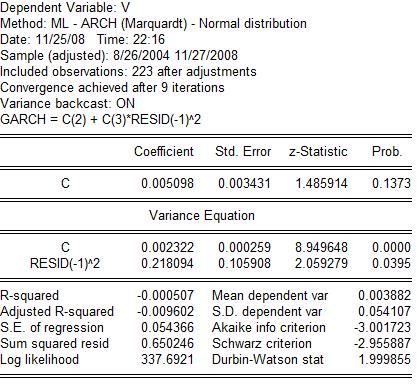

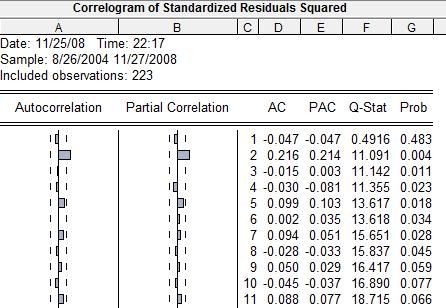

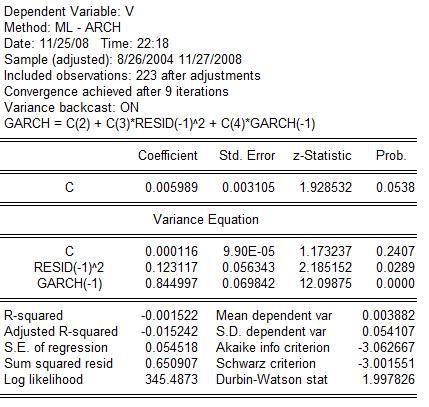

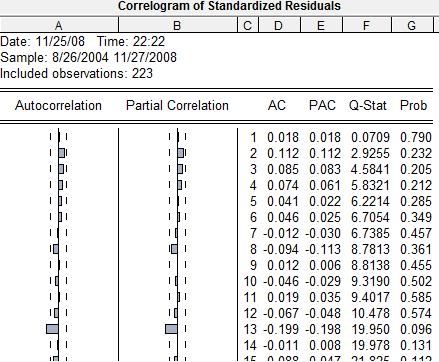

- Rezíduá a ich Q-štatistiky sú v poriadku.